“Liquidity” vs “solvency” in bank runs

and some notes on Silicon Valley Bank

Originally posted to LessWrong.

epistemic status: Reference post, then some evidenced speculation about emerging current events (as of 2023-03-12 morning).

A "liquidity" crisis

There's one kind of "bank run" where the story, in stylized terms, starts like this:

- A bank opens up and offers 4%/ann interest on customer deposits.

- 100 people each deposit $75 to the bank.

- The bank uses $7,500 to buy government debt that will pay back $10,000 in five years. Let's call this "$10,000-par of Treasury notes", and call that a 5%/ann interest rate for simplicity. (Normally, government debt pays off a bit every month and then a large amount at the end, but that's just the same thing as having a portfolio of single-payout (or "zero coupon") notes with different sizes and maturity dates, and the single-payout notes are easier to think about, so I'm going to use them here.) We're going to assume for this entire post that government debt never defaults and everyone knows that and assumes it never defaults.

- The thing you hope will happen is for every depositor to leave their money for five years, at which point you'll repay them $95 each and keep $500—which is needed to run the bank.

- Instead, the next week, one customer withdraws their deposit; the bank sells $100-par of T-notes for $75, and gives them $75 back. No problem.

- A second customer withdraws their deposit; oops, the best price the bank can get for $100-par of T-notes, right now after it just sold a bit, is $74. Problem.

- But next week, let's say, it would be possible to sell another $100-par for $75 again.

At this point, the simplified bank is stuck. If it sells ~$101-par of T-notes to return the $75 deposit, it won't have enough to pay everyone else back, even if the withdrawals stop here! But if it doesn't give the depositor back $75 right now, then bad things will start to happen.

Equity capital: A liquidity solution

So, we fix this problem by going back in time and starting with an extra step that's now required by law:

- Before taking $7,500 of deposits, the bank has to raise 10% of that—so, $750—of what we'll call "equity capital". Equity capital will get used to fill the gap between asset sales and returned deposits

Now, the final step of the original story goes differently:

- $1 of equity capital, plus the $74 from the T-notes sale, go to repaying the withdrawn deposit.

- Now the bank has 98*$75 of deposits, and $749 of equity capital. If nothing happens until next week (when the T-note price will go back to $75), everything will be fine. (In fact, the bank now has 10.19% of deposits in equity capital, making it safer then before.)

- A third customer withdrawal forces the bank to sell another $100-par of T-notes at $73, and use $2 of equity capital to repay the deposit. Now the bank has $747 of equity capital, 97*$75 of deposits, and a equity-to-deposits ratio of 10.27%.

- A fourth customer withdrawal forces the bank to sell another $100-par of T-notes at $72, and use $3 of equity capital to repay the deposit. Now the bank has $744 of equity capital, 96*$75 of deposits, and a equity ratio of 10.33%.

Even as the withdrawals force the bank to sell T-notes for greater and greater losses (relative to the $75 that the price will go back to next week), the equity ratio stays above 10%.

Until...

- [...]

- The fourteenth customer withdrawal forces the bank to sell another $100-par of T-notes at $62, and use $13 of equity capital to repay the deposit. Now the bank has $659 of equity capital, 86*$75 of deposits, and a equity ratio of 10.22%.

- The fifteenth customer withdrawal forces the bank to sell another $100-par of T-notes at $61, and use $14 of equity capital to repay the deposit. Now the bank has $645 of equity capital, 85*$75 of deposits, and a equity ratio of 10.12%.

- The sixteenth customer withdrawal forces the bank to sell another $100-par of T-notes at $60, and use $15 of equity capital to repay the deposit. Now the bank has $630 of equity capital, 84*$75 of deposits, and a equity ratio of 10.0%.

...and here is where the oops happens. Still, we're much better than the original case, as this bank with an initial 10% equity ratio can weather up to 16% withdrawals in a week, and if it sees anything less than that, it actually comes out stronger (in terms of capital ratio) by the next week when T-note prices reset.

[This is where I'd like to have an interactive chart about deposit withdrawals and their effect on capital position. But the speed premium to getting the post out is too high, alas.]

Furthermore, when the seventeenth depositor asks for a withdrawal, there's a very-reasonable case to be made to say "everything is fine; our equity ratio is still 10%; you can have your money back next week if you want, but right now is just a very bad time, could you possibly reconsider". And if they do hold off, they'll be fine!

If they ask for it anyway, then you give it to them, use $16 of equity capital, and you quickly find a new equityholder to put in another $8.5 of equity capital to get back to 10% equity ratio.

But, if your moral suasion and willingness to pay the seventeenth withdrawal stops the eighteenth and subsequent, then you, like George Bailey, can stop the run on your bank.

And if you do make it to next week (when we assume T-note prices reset), everything is fine (with the deposits at least—your equityholders lost some money, but that's the risk they signed up for).

We'll call this kind of situation a "liquidity crisis".

A "solvency" crisis

There's a different kind of "bank run", which is worse than the first kind. The stylized story starts like:

- (Interest rates are currently 1-2% annualized.)

- You raise $900 of equity capital.

- You open the bank and offer to pay 1%/ann on deposits. (The Very Large Bank down the road is paying 0.01% on deposits, so this attracts customers.)

- 100 people each deposit $90 to the bank.

- The bank uses $9,000 to buy $10,000-par of T-notes maturing five years from now (for a 2%/ann simple interest rate).

- You hope to repay a total of $9,500 five years from now and use $500 to run the bank.

- Three months later, a faraway cabal of wizards announce that interest rates on government debt will henceforth be 5%/ann instead.

- A competitor opens a bank that offers to pay 4%/ann on deposits.

- A customer comes to you and says "Look, Mr. Bailey, my family has always banked here, but your deposit rate is just so much lower than the new bank next door. If you can raise your interest rate on deposits to just, say, 3%/ann, I'll be willing to give up the extra 1% just to keep banking with you. But I can't give up 3% for the relationship; I just can't."

Okay, so now you have a real problem.

Non-option 0: Hope for rates to go down

- Give this customer their withdrawal.

- Do some fancy accounting to make it look like everything is okay.

- If rates go back down, everything can go back to the way it was before.

- Otherwise, it just gets worse by the day.

Not a real option, then.

Non-option 1: Maintain rates

- With a tear in your eye, you tell the customer you can't raise deposit interest rates...

- ...so they withdraw their $90. You sell $100-par of T-notes at $75 (that's what 5%/ann yield means!), and use $15 of equity capital to make that depositor whole. Now the bank has $885 of equity capital, 89*$90 of deposits, and a equity ratio of 9.93%.

- You're in trouble.

How much trouble? Well, in order to be back in the position of the George Bailey bank with respect to deposits (except 20% larger), you'll need an extra $15 in fresh equity capital for each depositor, or another $1,500 total.

- Problem 1: If you raise another $1,500 of equity capital, the new equityholders will own 15/(15+9)=62.5% of the bank. Bad news for the existing equityholders.

- Problem 2: Raising $1,500 of new equity capital will put you in the same position as the George Bailey bank. But if GB Bank needed $900 of equity capital to take $9,000 of deposits, then an investor could pay $900 to own 100% of GB Bank equity. Why would they pay $1,500 to own 62.5% of you instead?

Even if you offered to sell them the bank for the price of one Snickers bar, on the condition that they put in the $1,500 to make it whole, that's still a worse deal for them than them buying into GB Bank. So you have a big problem, starting from the very first withdrawal.

Non-option 2: Re-float rates

- With a glint of steely resolve in your eye, you commit to paying 3%/ann on deposits.

- Now, over the next 5 years, you'll owe $1,000 more in (simplified) interest than you had planned.

- You only have $900 of equity capital, and in any case you need all of that (and really, you need much more) to cushion against deposit withdrawals.

- So you consider selling the bank. But even at a price of one Snickers bar, no buyer wants to also put in the $1,000 they'd need to cover the higher interest on deposits—why would someone put in $1,000 to own your bank when they could put in $900 to own one that's safer from the effects of withdrawals?

So basically, by the time you've (1) collected deposits, (2) invested them all in 5-year T-notes, and (3) interest rates go from 2% to 5%? You're already in trouble. You're already underwater. Your 10% equity capital is not close to sufficient, and in theory you shouldn't be able to find anyone willing to take your bank from you, even at the price of one Snickers bar.

This is different from the liquidity crisis above! In the liquidity crisis, everything is fine if your depositors make one withdrawal a week in an orderly fashion.

In what we'll call a "solvency crisis", even if one withdrawal happens per week, you will still collapse long before they're finished. Unless you can somehow convince your depositors to stay for the whole five years and accept the 1%/ann interest rate the whole time, in which case you will be okay. You can hope, but that's not really a thing that should happen, especially if people know what's going on.

Your only option is...

Option 3: Liquidation

- With a sinking pit in your stomach, you call the Federal Deposit Insurance Corporation (which you can think of as basically an arm of the government).

- They take over the bank on Friday afternoon.

- Over the weekend, the government lends the bank $1,600 temporarily.

- On Monday the FDIC-controlled bank lets every depositor take out $25, which they all do. (In real life, this number is $250,000.)

- Now there's no more equity capital in the bank, just the T-notes. But depositors can't withdraw any more, so this is temporarily fine.

- Next, the FDIC controller comes up with a plan for selling the T-notes. They are extremely good at this and somehow sell them all for $73 per $100-par over the next three months.

- They repay the $1,600 government loan.

- Now there's $5,700 of cash and $6,500 of "uninsured" deposits. Depositors can withdraw $57 for every $65 of remaining deposit—in the end, they've gotten $82 out of their original $90 back. This is not good.

In real life, this is not what the FDIC will actually do. Instead:

Option 4: Acquisition

- They take over the bank on Friday afternoon.

- Over the weekend, the government lends the bank $1,600 temporarily.

- On Monday the FDIC-controlled bank lets every depositor take out $25, which they all do. (In real life, this number is $250,000.)

- Now there's no more equity capital in the bank, just the T-notes. But depositors can't withdraw any more, so this is temporarily fine.

- Next, the FDIC controller comes up with a plan for selling the bank. They call up a very large bank with $9 million of deposits and say "Can you please consider buying this bank over here for the price of one Snickers bar, plus a promise to make it whole?".

- Going unsaid in this conversation is "And, if you do this for us as a favor, we'll be 1% nicer to you across your entire business for the next three years."

- The Very Large Bank says yes of course we will do our patriotic duty, and, announces with great solemnity that for the good of the whole financial system it will buy the distressed bank for the price of one Snickers bar and make it whole.

- They check under their couch cushions and find $2,250, repay the government loan, and put $650 into fresh equity capital. They sell $1,800-par of T-notes for $1,350—leaving $82-par for every $65 of deposits, to cover their deposit interest.

- Very Large Bank announces: you're depositors with us now, you can withdraw your remaining $65 now if you like, but also *gestures around* you probably won't need to do that.

- The depositors mostly shrug and leave their money where it is. Some of them withdraw it to put it elsewhere, but VLB can manage that.

This ends up costing the Very Large Bank $900 and a bit of headache to own a bit more bank that's presumptively worth $650. But they enjoy the slight favor of their regulators for the next few years, across their whole business, which is worth far more to them than anything else in this story.

Taxpayers never end up with the bill for "bailing out" the bank, which is good politics. (The negotiated takeover is sometimes called a "bail in", which only makes sense if you don't think about it.)

Depositors were allowed to withdraw $25 immediately (from the FDIC-controlled bank) and $65 later (from Very Large Bank post-takeover). Plus interest from the time the money was in limbo, which I've been ignoring for simplicity. They're fine.

Silicon Valley Bank

The consensus narrative (at this time - 2023-03-12 morning) about Silicon Valley Bank, the sixteenth largest bank in the US, is that it faced a solvency crisis based on investing in long-term government debt and something called Agency MBS (which you can just read as "government debt with extra steps"). The FDIC has taken over, and will presumably follow Option 3 or Option 4.

Some of the coverage has focused on liquidity elements of the crisis, but my understanding is that the shock to liquidity merely forced the realization that SVB was insolvent sooner than it would have otherwise; it didn't change the inevitable facts of insolvency.

Liquidity: Okay until it's not okay

Like many solvency crises, it was possible to ignore it for a time after the rates moved, while there was sufficient liquidity, because (1) there weren't material amounts of withdrawals, (2) interest rates paid on deposits were slow to catch up to debt-market rates, and (3) no one was looking very hard ahead of the hockey puck for something like this at a bank with less than $250 billion of deposits (when some different regulatory rules kick in).

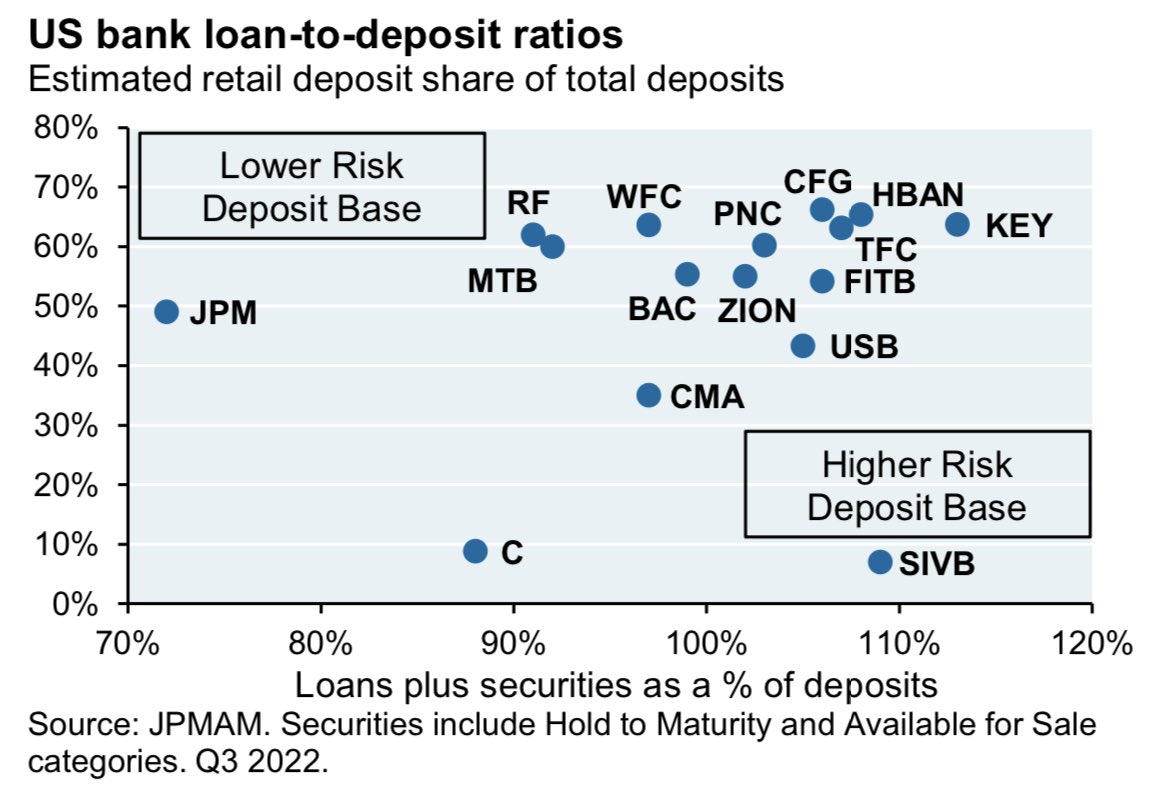

Regarding (1), we can start with the fact that SVB's deposit base was less than 10% retail deposits made by individuals:

Retail depositors, like most humans, are often looking to minimize contact with their bank as much as possible, and it's not crazy to think that they might stick around even if your interest rate is a few percent worse, or there's some concerning news but it uses a bunch of financial jargon and is hard to understand. Besides, if $250,000 of your deposits are going to be available on Monday in the case of an FDIC takeover, and you have less than that on deposit, why bother?

On the other hand, if you're a professional CFO making decisions for a corporate business, you deal with your bank all the time. You read the news. And if you and all the other CFOs all ready the same bad news, you might collectively withdraw $42 billion from your accounts in one day.

Even worse, SVB was the bank of choice for much of the Silicon Valley startup scene (I've seen estimates of 30% of companies and higher in biotech). This was good business when net deposits were positive every year for many many years, until mid-2022 when that stopped being true. Unfortunately (but not unforeseeably), a sudden industry-wide stop in inflows into startups can be caused by interest rates rising, which made SVB's book of startup deposits and long-term debt doubly vulnerable to interest-rate rises—the liquidity crunch comes exactly when your solvency takes a turn for the worse.

Still, all of this action on point (1) poses a liquidity issue, not a solvency issue. SVB could have had no depositor flight at all—as in Option 2—and still taken a controlled flight into terrain.

The reasons for (3) could be a whole 'nother post, but my understanding is that a material contributor was that the accounting rules (which every bank uses!) allowed SVB (like every other bank with assets <$250bln) to take most of the assets that it had bought at 90¢, and which were now trading 75¢, and treat them as being still worth 90¢ when calculating the amount of assets available to repay deposit withdrawals. This is called "hold-to-maturity", and the rules about when you can and can't apply it are more complicated than this post can contain.

(In)solvency: Why, and where else?

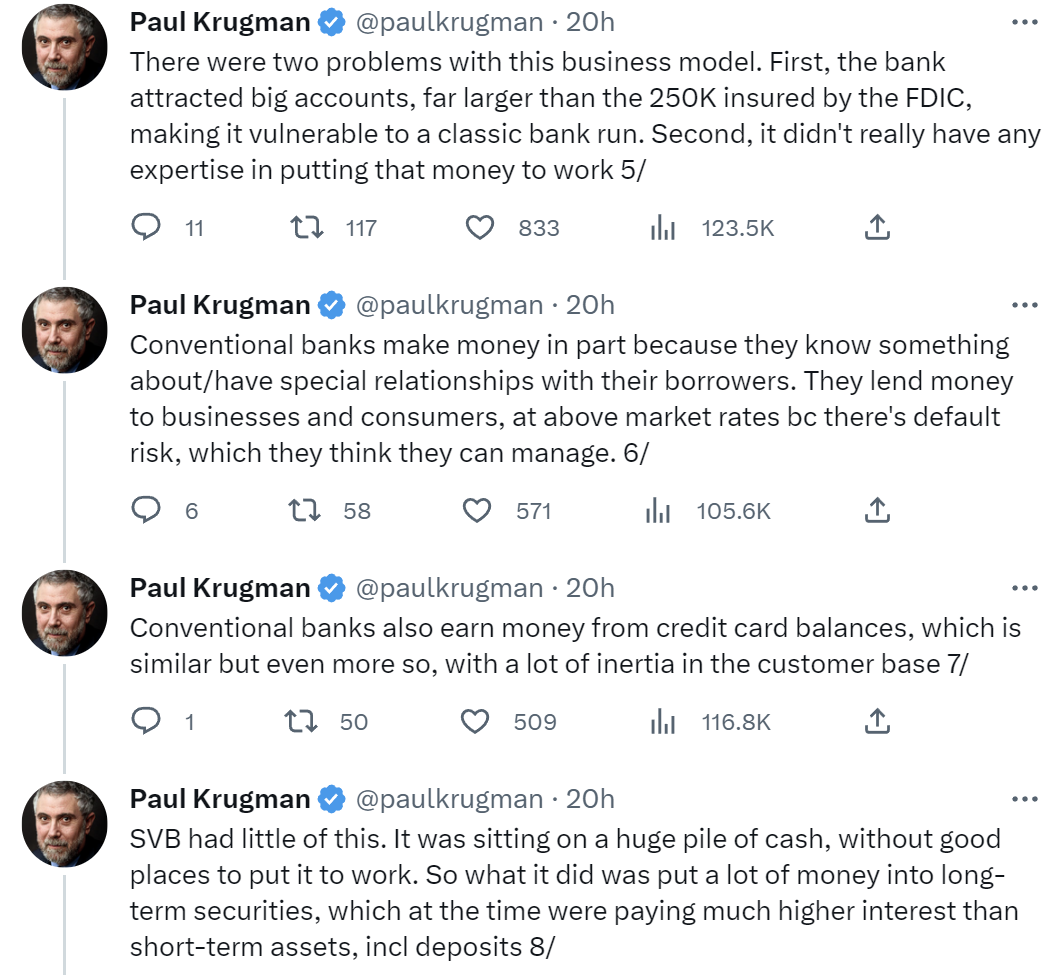

Okay, but if solvency is the big issue, then why did SVB end up with an asset book so exposed to interest rates? Should we expect similar performances from other banks? Paul Krugman has a theory, which seems pretty solid to me:

Matt Levine has a similar take:

Or, to put it in different crude terms, in traditional banking, you make your money in part by taking credit risk: You get to know your customers, you try to get good at knowing which of them will be able to pay back loans, and then you make loans to those good customers. In the Bank of Startups, in 2021, you couldn’t really make money by taking credit risk: Your customers just didn’t need enough credit to give you the credit risk that you needed to make money on all those deposits. So you had to make your money by taking interest-rate risk: Instead of making loans to risky corporate borrowers, you bought long-term bonds backed by the US government.

In this model of the problem, the least concerning shape of bank in the present environment is one that gets its lending profits from short-term loans to businesses that are risky, but manageably so. If you were good at this kind of thing, I'm sure there were plenty of small businesses that were looking for 2-year bank loans, and if you can find the good ones and charge them 8% above prime and have 6% losses to defaults, then you can turn a profit without taking interest rate risk.

The most concerning shape of bank right now, on the other hand, is one with no on-the-ground lending operations, whose only ability to lend cash and collect interest came from things you could find on a Bloomberg terminal (or in places that themselves took a bath on rising interest rates). Those banks, when they needed slightly higher interest rates, had little choice but to reach for yield by taking things that were (a) lower-credit, (b) longer-duration, or (c) exposed to other risks that recently got toasted. (a) is a well-known problem, and presumably was off the table due to regulatory constraints. But if SVB managed to pile up enough (b) and (c) to get into trouble, are there other banks with little community lending in the same situation?

I don't do this professionally, but I'm interested to find out. We'll see more on Monday.

Edited to add some recommendations from the comments, but I'm not going to update this article for things that happened after midday Sunday, March 12.